In this article we will go through the following:

- Super is not an investment

- Super’s sole purpose

- Tax concessions

- Preservation

- What happens at retirement?

You might not believe me, but ‘superannuation’ derives from the medieval Latin word superannuatus, which literally means ‘to be too old’. True. While that might not be the best way to start this article, it does at least provide a clue to the simple steps.

1. SUPER IS NOT AN INVESTMENT

Instead, it is an invest-OR . Superannuation funds invest in things like bank deposits, shares, property, etc. – just like any other investor (be it an individual, a trust or a company).

We often hear people say, ‘super gives a lousy return’, when, in fact, super does not give a return at all. It is the things that the super fund invests in that provide the return.

So, what’s the difference between investing through a super fund, as opposed to investing directly or through a trust or something of the like? I’m glad you asked…

2. SUPER’S SOLE PURPOSE

Superannuation can be thought of as government-sponsored saving. The Government (on behalf of us taxpayers) has a vested interest in encouraging people to save for their own retirement. Offering generous tax concessions now encourages us to save, so we can at least partially fund our own retirement. This reduces the future burden on the public purse through Age Pensions and the like.

But, the deal is, superannuation must be used for the sole purpose of providing retirement benefits for fund members and their beneficiaries. So, if we can’t use it now, what’s the incentive?

3. TAX CONCESSIONS

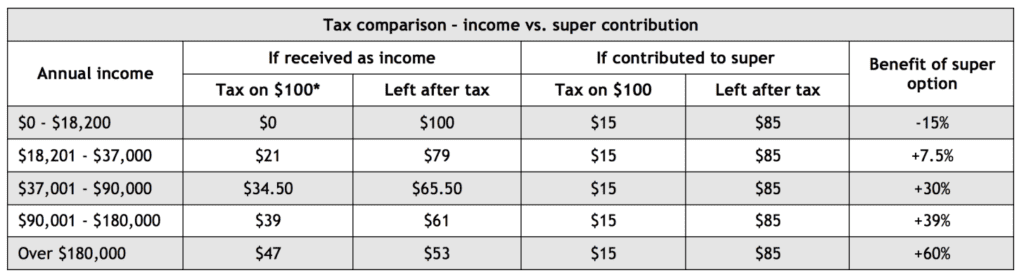

Put simply, if you are earning an income over about $20,000 per annum, then super is the best game in town for legitimately minimising tax on your savings. Do not believe anything to the contrary. To illustrate, the table below shows how much better off you are to make super contributions instead of receiving the money as taxable income, at various levels of income:

*Includes Medicare Levy. Excludes Mature Age Workers Tax Offset and Temporary Budget Repair Levy

Super is your best bet from a tax viewpoint and should be at the heart of your financial plans.

‘Generous tax concessions from the Government…surely this is too good to be true?!’ I hear you…

4. PRESERVATION

You’re kind of right. You don’t get access to these generous tax concessions for nothing.

Your part of the deal is that funds invested in super are intended for your retirement, and there are restrictions in place designed to limit access to your funds until then.

5. WHAT HAPPENS AT RETIREMENT?

Once you reach retirement* you can access your funds freely. While this could be by way of tax-free lump sum withdrawals, there are strong incentives in place to simply leave your money invested in the fund and instead draw regular income payments. This is called a pension – note: it’s a superannuation pension as opposed to the Age Pension.

*NOTE: ‘retirement’ looks different for everyone and can take place at different times depending on circumstances. It is important to be aware of certain age restrictions that need to be met in conjunction with retirement in order to ‘access your funds freely’ – referred to as ‘Preservation Age’.

A QUICK WORD ON RULE CHANGES – ARE THEY REALLY WORTH WORRYING ABOUT?

It’s true that the rules are forever being tweaked but note that they have never eliminated the tax advantages of super.

Super is the main instrument of the Retirement Income Policy, and while there exists the will to assist people to save for their retirement, super will always be attractive relative to other alternatives.

And that’s about it! No need to make it more complex than it needs to be.

Use superannuation for its intended purpose and it really is a very good deal